Latest News

-

June 4, 2026

June 4, 2026BESS in India: Advait Records Highest Revenue Jump | NDTV Profit

-

May 17, 2026

Where is the project located | Green Hydrogen | Locations | Advait Greenergy | Advait Group | AGPL

-

May 5, 2026

Building Advait Greenergy — India's Clean Energy Story | Rutvi Sheth Kundalia | AGPL | Advait Group

-

April 29, 2026

Where Every Electrolyzer Earns Its Place in India's Green Hydrogen Mission | Advait Greenergy

-

April 28, 2026

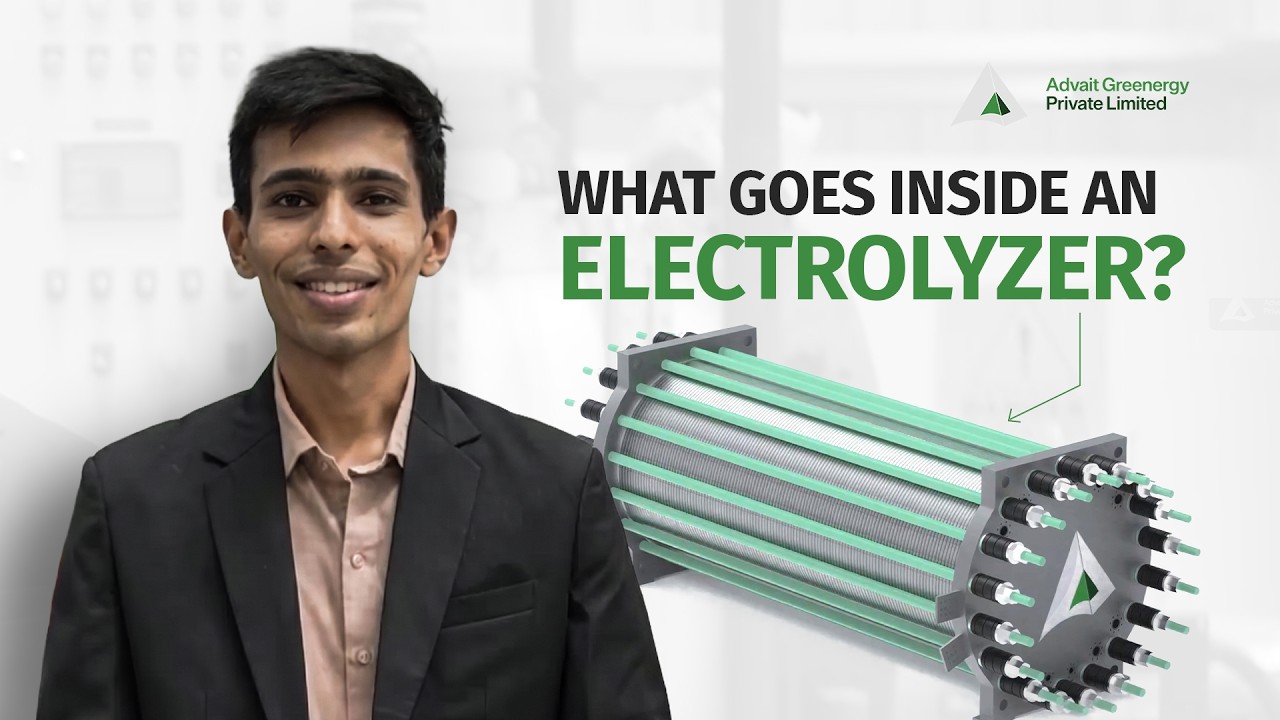

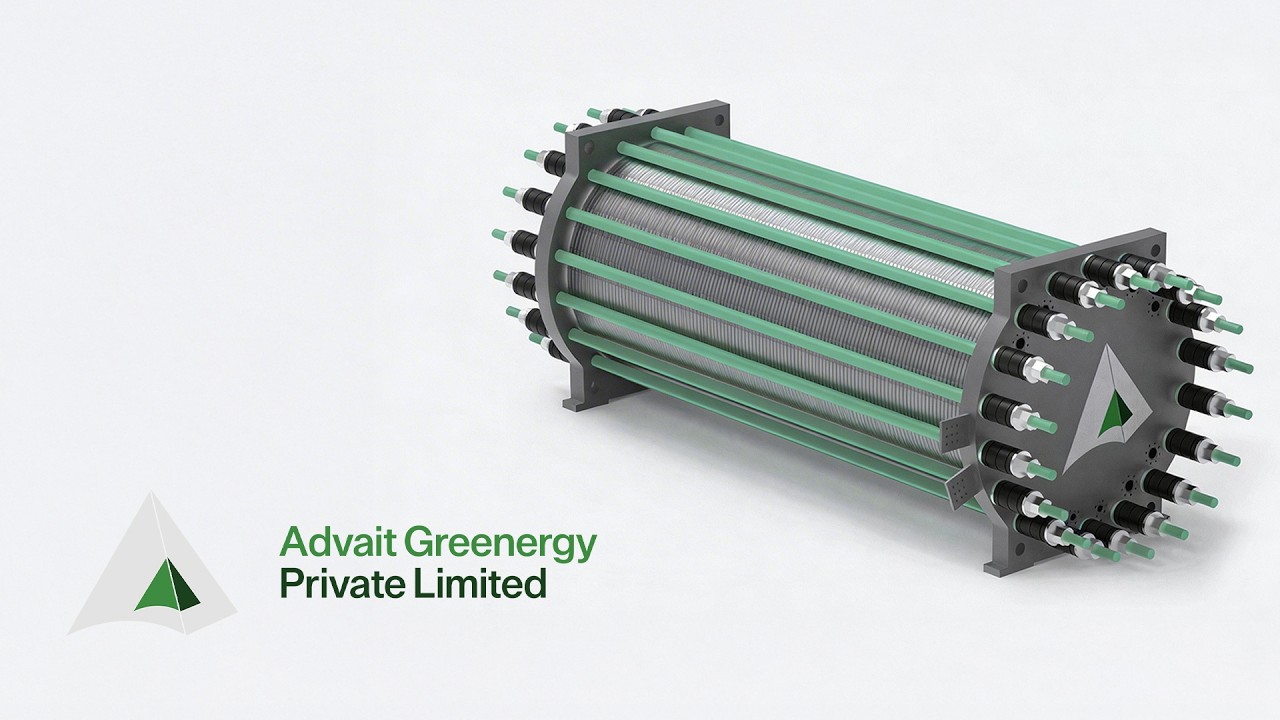

What goes inside an electrolyzer | Advait Greenergy | AGPL | Advait Group

-

April 27, 2026

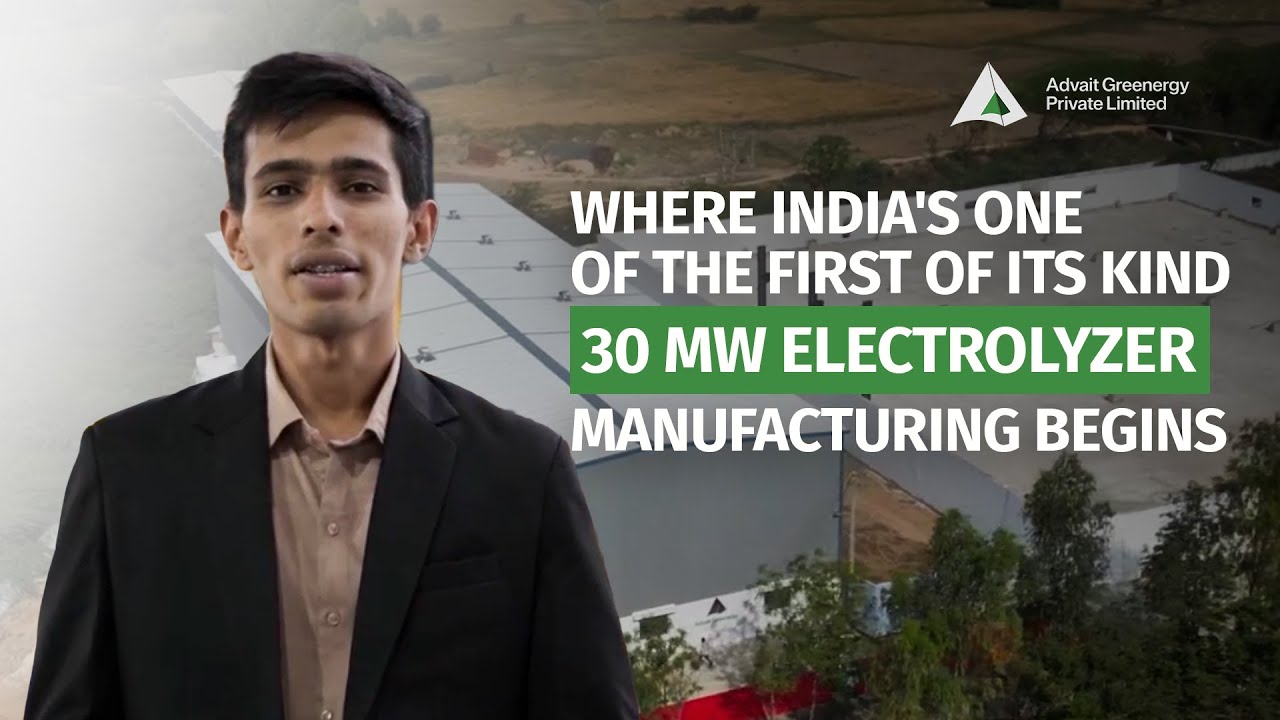

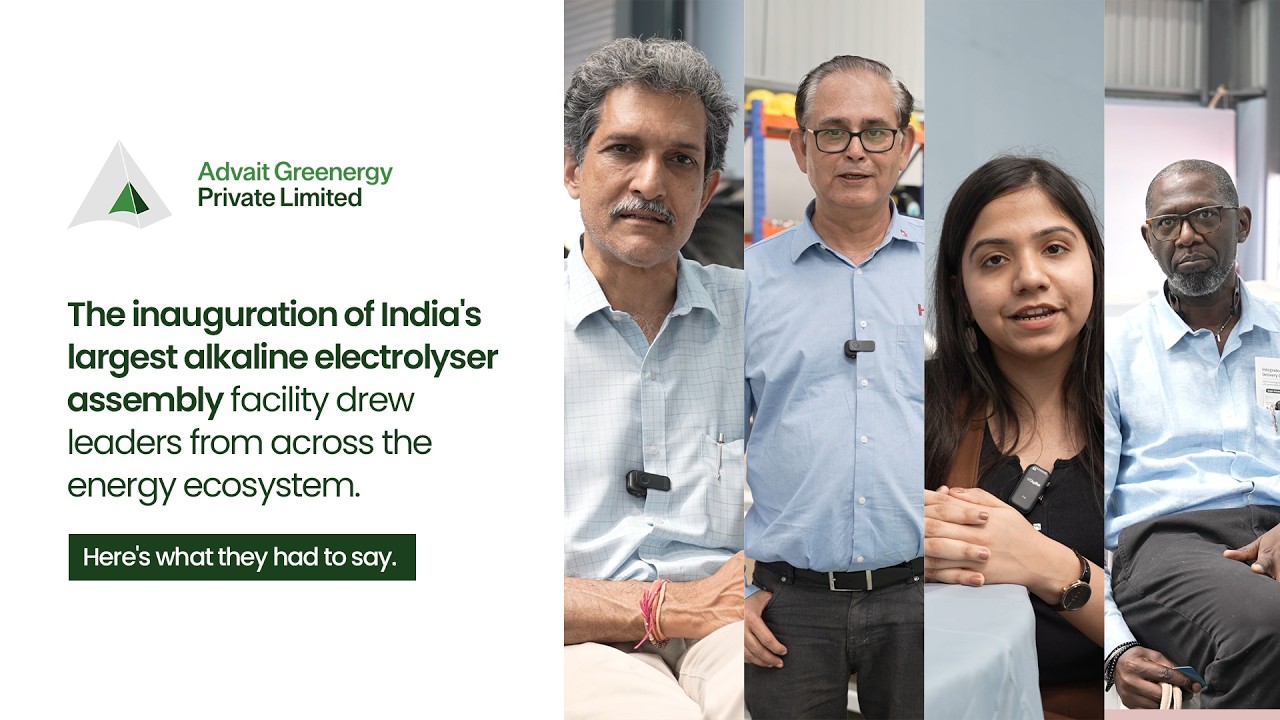

Inside India's One of the First 30 MW Alkaline Electrolyser Assembly Line | Part 1 | Advait Group

-

April 21, 2026

Somewhere between commissioning day and the first BESS tender | Advait Greenergy | AGPL | Advait

-

April 20, 2026

Where does green hydrogen actually make sense first? | Advait Greenergy | AGPL | Advait Group

-

April 18, 2026

Grey Hydrogen vs Green Hydrogen | Advait Greenergy | AGPL | Advait Group | Advait Energy | AETL

-

April 13, 2026

A quiet shift happened recently in New Delhi, and it didn’t get the attention it deserves | Advait

-

March 28, 2026

One of India's First 30MW Alkaline Electrolyser Assembly Line | AGPL | AETL | Advait Group

-

March 27, 2026

India's one of the first 30 MW alkaline electrolyser assembly line | Advait Greenergy | Advait Group

-

March 17, 2026

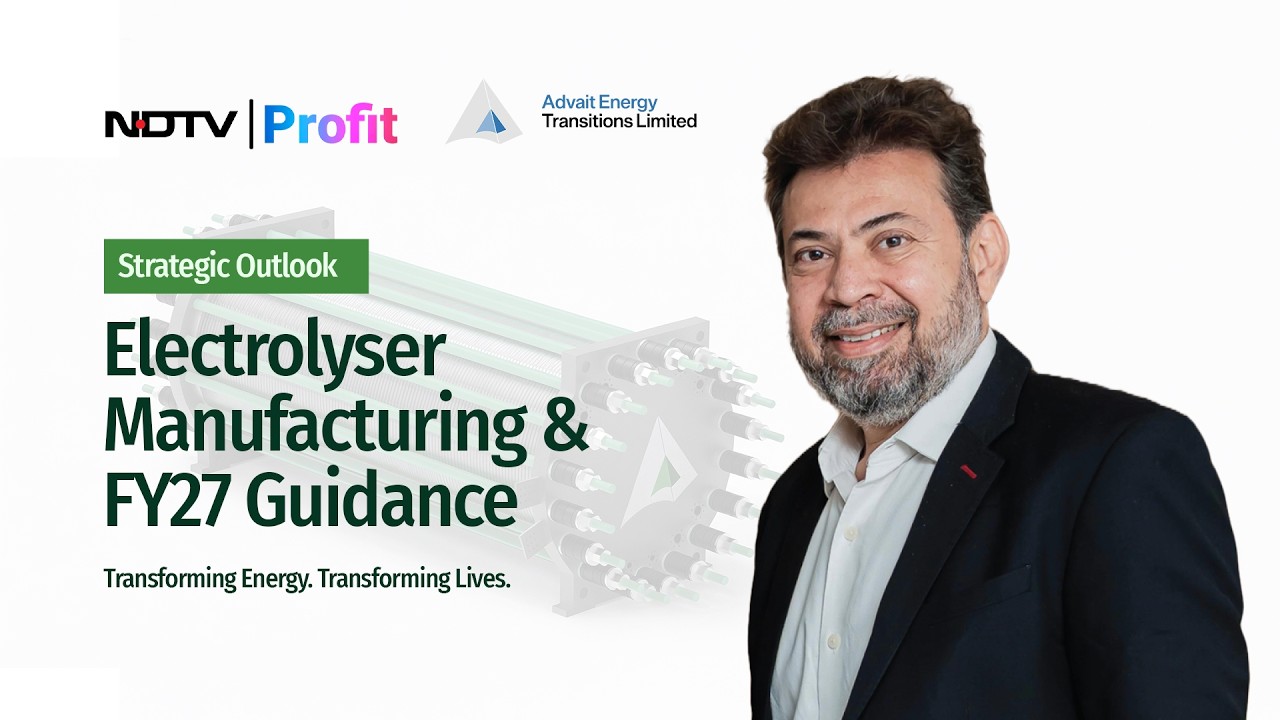

Strategic Outlook: Electrolyser Manufacturing & FY27 Guidance | Advait Energy Transitions Ltd.

-

March 13, 2026

Evolution of AGPL | Past, Present, and Future | Advait Group

-

February 5, 2026

February 5, 2026Why corporate relations will define the green energy future

-

February 5, 2026

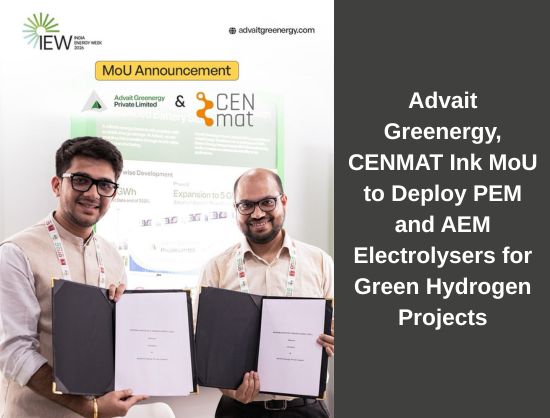

February 5, 2026Advait Greenergy, CENMAT Partner to Scale Green Hydrogen Projects with PEM and AEM Electrolysers

-

February 4, 2026

February 4, 2026Advait Energy Transitions Limited's (NSE:ADVAIT) Popularity With Investors Is Clear

-

January 29, 2026

Budget 2026: Vatsal Kundalia Deep Dive into Budget 2026 Energy Needs.

-

January 22, 2026

January 22, 2026Budget Expectation

-

January 22, 2026

January 22, 2026Why Corporate Links Are Key To The Green Energy Shift

India’s Battery Energy Storage Ambition Faces A Reality Check

COVER STORY: India’s Battery Energy Storage Ambition Faces A Reality Check

Low bidding prices and a rising volume of tenders have masked a rising risk to India’s energy storage ambitions. The risk of disruption from rising input prices.

* Several solar and BESS developers in 2025 bagged several storage-related projects at record tariffs, most of them first-timers.

* With more standalone BESS and solar+BESS tenders and avenues, India also witnessed a rise in BESS component manufacturers

* But how can the new rising industry, far more complex than solar, overcome the multiple challenges it faces?

The Indian renewable energy market is now undergoing a transition phase vis a vis energy storage. For long considered the vital bridge that will enable the market to move from a 20% wind + solar combination to over 40%, the sharp drop in storage prices over the past two years raised hopes that the best case scenario for storage additions would be achievable on time after all. Now, after the initial years of pilot projects and an exploratory phase, the battery energy storage system (BESS) market in India is finally taking its first steps towards scalability.

Several tenders floated in 2025 attracted headline-grabbing low tariffs for storage projects. If 2025 was about tenders and the lowest-ever tariffs, 2026 is expected to be a testing ground for real on-ground execution and learnings.

Fate Of BESS Projects In 2025

In 2025, Madhya Pradesh grabbed national attention when the Morena solar-plus-storage project, with two hours of battery storage, discovered a tariff of ₹2.70/kWh, one of the lowest ever for such projects in the country.

In the same year, standalone tenders for two-hour battery energy storage systems (BESS) saw tariffs fall to a historic low of ₹1.48 lakh per MW per month. Meanwhile, firm and round-the-clock renewable energy (FDRE/RTC) projects were awarded at tariffs largely clustering in the ₹4.3–₹5.1/kWh range, depending on the tender structure and counterparty. A far cry from the Rs 8 plus prices discovered just 15-18 months earlier.

The current surge in BESS projects closely mirrors India’s early solar journey, when key components were heavily dependent on offshore markets, the technology was still evolving, skilled manpower was limited, and China dominated large parts of the global supply chain.

A similar pattern is now evident in energy storage. Indian BESS manufacturers remain almost entirely dependent on China for lithium-ion cells and several critical components, echoing the vulnerabilities that once characterised the solar sector during its formative years.But BESS manufacturing and its project implementation is a completely different ballgame and far more complex than solar projects or solar module manufacturing. Thus, it will demand a lot more effort.

Ratings and research firm ICRA said that a significant decline in battery costs over the past decade has helped reduce the cost of energy storage and adoption of BESS projects globally. Based on prevailing battery costs, ICRA estimates that the levelized cost of storage using BESS for 2-4 hours of storage is relatively high, in the range of Rs. 4.0-7.0 per unit, compared to Rs. 5.0 per unit for Pumped Storage Hydropower (PSP) projects. This has seen a significant improvement from the level of over Rs. 8.0-9.0 per unit seen in 2022. While BESS costs for 4-hour storage remain higher than that of PSP, the execution risks and gestation period for the BESS projects are much lower, by as much as 36 months.